In this post, I am going to teach you that what are capital budgeting techniques, how net present value, profitability index, payback period, internal rate of return can be calculated & how all these put impact on investment criteria.

Introduction to Capital Budgeting Techniques

Net Present Value and other Investment Criteria such as Internal Rate of Return, Payback Period, and Profitability index are different concepts of Capital Budgeting Techniques. These all deal with future investment proposals. With the help of all the above techniques, we decide either to choose the project or leave to invest in the project.

Among all four above, Net Present Value and Internal Rate of Return are the two most common primary ways to estimate future profitability and these both have very important relations with each other which will be discussed later in this topic whereas profitability index and payback period are both secondary ways to assess the profitability.

Net Present Value NPV

Net present value is simply the net sum of present values of cash outflow or initial investment and future cash inflows. Cash outflow is our investment which we plan to invest in a certain investment proposal and cash inflows are those inflows that we expect to earn in the future for a certain time period.

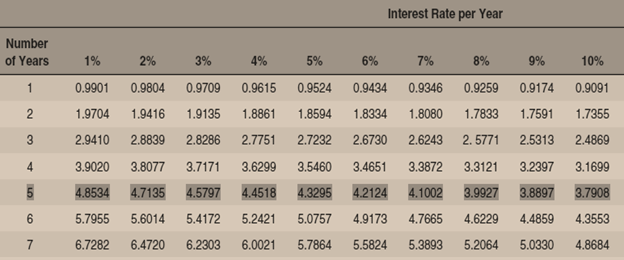

For the calculation of net present value, we have to understand present value calculation by using present value tables or manual calculation. One thing you should remember is that if future cash inflows are same, then you can use the Present Value of Interest Factor of Annuity (PVIFA) otherwise Present Value Interest Factor PVIF.

Present value has vital importance in the concept of the time value of money which tells us that how much value is today for future cash flow because there are various factors those minimizes the value of money as time passes.

Acceptance Criteria of Investment under Net Present Value

If NPV = 0 means no profitability no loss

If NPV > 1 means profitability

If NPV < 1 means loss

Net Present Value Formula for Similar Cash Inflows:

Net Present Value Formula for No similar Cash Inflows

The formula for PVIFA Present Value of Interest Factor of Annuity

Formula for PVIF Present Value of Interest Factor

Calculation of NPV with Similar Cash Flows

Practical Questions for Understanding

Question 1: If opportunity cost of capital is 10%, Calculate NPV of both projects, In case of mutually exclusive projects, which project is better to invest?

| Year | Project A | Project B |

| 0 | -500 | -500 |

| 1 | 400 | 450 |

| 2 | 400 | 450 |

| 3 | 400 | 450 |

| 4 | 400 | 450 |

| 5 | 400 | 450 |

Solution:

Project B is worth more because NPV of Project B is greater than the NPV of Project A

Calculation of NPV with Non Similar Cash Flows

Practical Questions for Understanding

Question 2: Calculate Net Present Value for the following cash flows if opportunity cost is 15%.

| Year | 1 | 2 | 3 | 4 |

| Cash Flows | 2500 | 1500 | 2700 | 3000 |

Solution:

NPV Net Present Value (Decommission Case)

Practical Questions for Understanding

Question 3: A cement plant will cost to you  350 million a year for 16 years. After that period, it must be decommissioned at a cost of

350 million a year for 16 years. After that period, it must be decommissioned at a cost of  40,000 annually. It can instead buy a machine at a cost of

40,000 annually. It can instead buy a machine at a cost of  11,000. The machine will be sold at the end of 5 years for

11,000. The machine will be sold at the end of 5 years for  5,000 a year to maintain. For

5,000 a year to maintain. For  2,000 a year.

2,000 a year.

a. If the discount rate is 4% per year, should you replace the forklift?

b. What if the discount rate is 12% per year? Why does your answer change?

Questions 2: Here are the cash flows for two mutually exclusive projects:

- Which project would you choose if the opportunity cost of capital is 2%?

- Which would you choose if the opportunity cost of capital is 12%?

- Why does your answer change?

Follow Book Corporate Finance BREALEY MYERS MARCUS

Question 3: Consider projects A and B:

Calculate IRRs for A and B. Which project does the IRR rule suggest is best? Which project is really best?

Question 4: A new computer system will require an initial outlay of  4,000 a year for each of the next 8 years. Is the system worth installing if the required rate of return is 9%? What if it is 14%? How high can the discount rate be before you would reject the project?

4,000 a year for each of the next 8 years. Is the system worth installing if the required rate of return is 9%? What if it is 14%? How high can the discount rate be before you would reject the project?

Question 5: Consider this project with an internal rate of return of 13.1%. Should you accept Project the project if the discount rate is 12%?

| Year | Cash Flows | ||

| 0 | + 2100 2100 | + 1200 1200 | |

| B | -2100 | +1440 | +1728 |

a. Calculate the profitability index for A and B assuming a 22% opportunity cost of capital.

b. Use the profitability index rule to determine which project(s) you should accept

To Follow the video lecture about Capital Budgeting Techniques click the link below:

To follow Statistics Blog Posts Click the link : https://bcfeducation.com/category/statistics/

To follow IGCSE/O Level Business Blog Posts Click the link : https://bcfeducation.com/category/business/

To follow Financial Management Blog Posts Click the link : https://bcfeducation.com/category/financial-management/

To follow IGCSE/O Level Accounting Blog Posts Click the link : https://bcfeducation.com/category/olevel-accounting/