Dive into the fundamentals of the Law of Supply, an essential principle in microeconomics. This blog post explores the relationship between price and quantity supplied, the assumptions underlying the law, and its practical applications in real-world market scenarios. Perfect for economics, business, and finance enthusiasts, this article breaks down the mechanics of supply, complete with examples and insights to help you grasp its significance in economic analysis. This topic is equally important for the students of economics across all the major Boards and Universities such as FBISE, BISERWP, BISELHR, MU, DU, PU, NCERT, CBSE & others & across all the business & finance disciplines.

Table of Contents

Law of Supply

Whenever producers increase the price of the product, they also increase the supply of the product to earn maximum profit. In contrast, when price of the product decreases, they reduce the supply of the product. So law of supply says that:

“Other things remaining the same, quantity supply of the product increases with increase in price and decreases with decrease in price”.

Here other things remaining the same means technology, cost of production, number of suppliers etc. are constant.

Relation of quantity supply and price can be expressed as:

Price of x ↑ Quantity Supply of x ↑ Price of x ↓ Quantity Supply of x ↓

Tabulated and Graphical Explanation

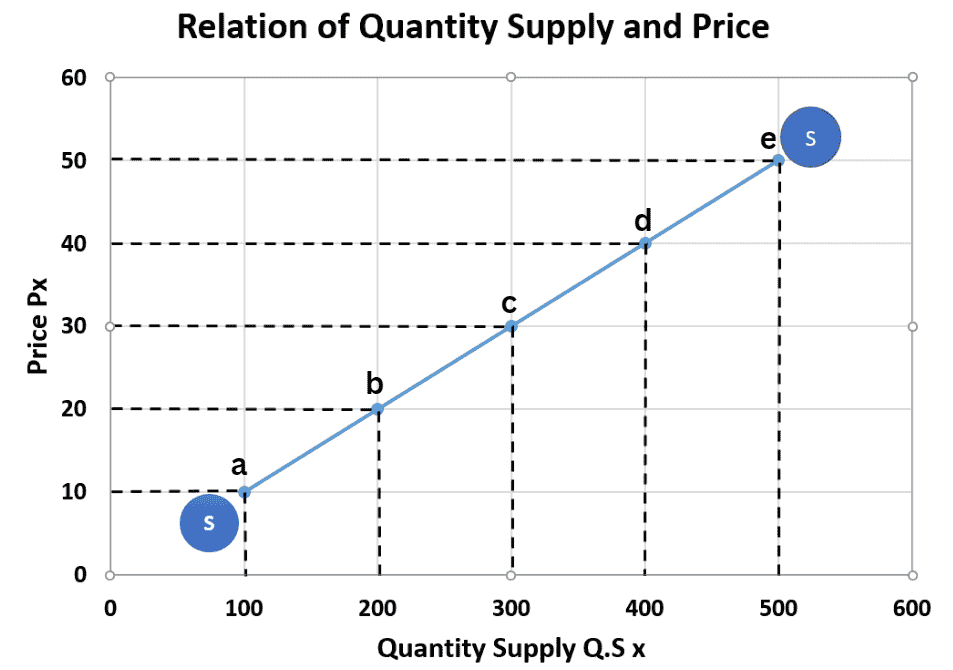

Table 4.1 Law of Supply

| Q.s (x) | P(x) |

| 100 | 10 |

| 200 | 20 |

| 300 | 30 |

| 400 | 40 |

| 500 | 50 |

Figure 4.1 Law of Supply

Explanation

Table 4.1 shows that as price increases, quantity supply also increases, which develops the positive relation between quantity supply and price. Positive relation between these two is also shown in the figure above that supply line is going upward from left bottom to right top. When price of the product is 10, its quantity supply is 100 units, similarly when price increases to 50, quantity supply also increases to 500 units. These points are shown in the figure above from point a to point e.

Assumptions

Ceteris Paribus

It is assumed that all other thing such as technology change, cost of production, number of suppliers & other factors remain constant other than price.

Perfect Competition

It is assumed that there is a perfect competition in the market which means there are many buyers and sellers and producers are free to enter and exit from the market.

Rational Behavior

Producer must be rational which means he wants to maximize profit through supply more at higher price.

No Change in Technology

It is also assumed that there is no change in technology because new technology also reduces the cost of production which leads to increase profits but that is not the case of supply and price.

No Government Intervention

It is assumed that there is no intervention of government because sometime government introduce subsidies, taxes, price controls and quotas which affect supply.

Short Run Analysis

The law typically applies to the short run, where the capacity of production is fixed, and firms can only adjust the quantity they supply by using existing resources more intensively.

No Anticipation of Future Price Change

Producers do not anticipate future changes in prices. If they expect prices to rise further, they might withhold supply to sell later at higher prices, contradicting the law of supply.

Limitations

Perishable Goods

Law of supply may not hold in case of perishable goods, because producers have to sell these goods even at lower prices to avoid spoilage.

Future Anticipation of Prices

Sometimes, producers anticipate future price hikes so they hold the supply to get more profit in future. In this way, the law of supply does not hold.

Government Intervention

Under government intervention of price ceiling, price floor, quotas, subsidies and taxes, the law of supply cannot be hold because this intervention restricts the law of supply to work independently.

Limited Resources

More resources are required to produce more goods to increase the supply so if resources are limited, the law of supply cannot be hold because of less supply.

Non-Profit Motivation

In some sectors, the major motivation may not be to earn more profit so under this condition, the law of supply ma not hold.

Unstable Economic Condition

Under unstable economic condition, producers sell their products even on less price so in this case, the law of supply fall in price results fall in supply does not hold.

Migration

Sometimes due to different reasons such as unstable economic conditions and hikes in inputs cost, producers want to move to other countries in search of favourable conditions, they sell their stock even on less price. So in this case, the law of supply falls in price results fall in supply does not hold.

Related Posts

Evolving different thoughts of Economics

2.1 Theory of Consumer Behaviour

2.2 Total Utility, Marginal Utility, Point of Satiety & Types of Utilities

2.3 The Law of Diminishing Marginal Utility DMU

2.4 The Law of Equal Marginal Utility EMU

3.1 Demand, Individual Demand, Aggregate Demand, Law of Demand

3.2 Change and Shift in Demand, Extension and Contraction in Demand, Rise and Fall in Demand